It was a positive week for equity markets that continue to shrug off the war in Iran. Bond markets are not quite so sanguine, with yields rising a bit on the latest inflation numbers from the US. Crude was up a few dollars, gold down a bit and Bitcoin up. All in all, a mixed week, but no one is rushing for the exits.

| Index | Close May 7th 2026 | Close May 14th 2026 |

| S&P500 | 7,333 | 7,506 |

| TSX60 | 33,857 | 34,268 |

| Canada 10 yr. Bond Yield | 3.53% | 3.56% |

| US 10 yr. Treasury Yield | 4.39% | 4.48% |

| USD/CAD | $1.36510 | $1.37249 |

| Brent Crude | $102.23 | $106.54 |

| Gold | $4,702 | $4,652 |

| Bitcoin | $79,942 | $81,635 |

Source: Trading Economics & Factset

Surprising no one, US inflation was higher in April rising to 3.8% year over year. This contrasts with the 3.3% reading in March and 2.4% readings in January and February. Energy costs accounted for about half of the rise, closely followed by food. Shelter costs were up as well, though there is some noise in these numbers. The data on shelter was skewed thanks to the government shutdown late last year. There is nothing in these numbers to warrant a rate cut and markets are giving a 60% probability to a rate hike in 2027.

Perhaps more concerning was the rise in the Producer Price Index (PPI) which rose to 6% year over year (5.2% core). Again energy was a big driver, but the services index also accelerated. Most of that move was attributed to trade services, another sign that tariffs are influencing prices. PPI is a precursor to changes in the Consumer Price Index (CPI)

None of this will make incoming Federal Reserve Chair Kevin Warsh’s job any easier. He was confirmed in his position by the Senate this week. He will now have to contend with rising inflation that may eventually call for rate hikes and a Whitehouse that has been consistent in its calls for lower rates. Warsh is only one vote on the rate setting committee (FOMC). He does have other plans for how the Fed operates, including reducing its balance sheet, reducing the number of monetary policy meetings, and not providing forward guidance.

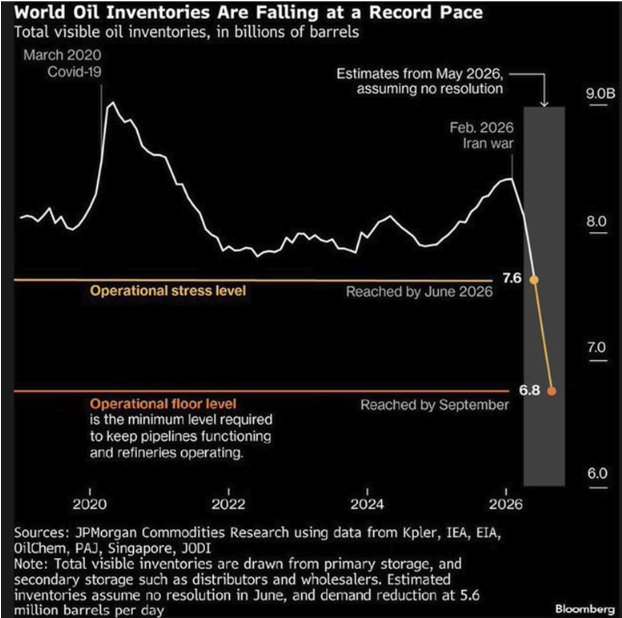

The longer the Strait of Hormuz remains closed, the worse this chart will get. World oil inventories are being drawn down at a prodigious rate. To be fair, the world was in a surplus position before the Iran war, we are seeing demand destruction, and supplies are being released from strategic reserves, so the full effect has not been felt yet.

Donald Trump and an entourage of America’s top business leaders travelled to Beijing this week. So far there has been pageantry, flattery, but not much of substance. China promised not to send military hardware to Iran but warned the US to not interfere with China’s claims on Taiwan. The US mission was more trade focused. Boeing managed to secure an order for 200 planes (less than expected) and Nvidia was given permission to export more of their H200 chips to 10 firms in China. So far, no chips have been shipped. China is more interested in utilizing their home-grown chips.

New/expanded “sovereign AI data centres” have been announced for Kamloops and Vancouver. The venture will be run by Telus and is in addition to 6 data centres either completed or planned by BCE. The projects are receiving federal government support under the “Enabling large-scale sovereign AI data centres” initiative. There is some pushback over concerns about water and energy usage.

It’s that time of the year again. This weekend will be the grand finale of the 2026 Eurovision song contest. The event will be filled with lights, music, crowds, and sequins. But we’ll let you tune in yourself to see it live. We’ll leave you with something a bit more classic from Led Zeppelin.

Russ Lazaruk, RIAC, CIWM, CIM, FCSI

Managing Director & Portfolio Manager

![]()