Another mixed week on the markets. The S&P500 was essentially flat again while the TSX continues its advance. Bond yields fell and are starting to bring US mortgage rates down with them. Oil prices declined marginally with a US strike against Iran still in the cards. Gold held over $5,000, supported by lower bond yields and its renewed safe-have status.

| Index | Close Feb 19th 2026 | Close Feb 26th 2026 |

| S&P500 | 6,866 | 6,897 |

| TSX60 | 33,595 | 34,502 |

| Canada 10 yr. Bond Yield | 3.24% | 3.17% |

| US 10 yr. Treasury Yield | 4.08% | 4.01% |

| USD/CAD | $1.37011 | $1.36673 |

|

Brent Crude |

$71.92 | $70.85 |

| Gold | $4,999 | $5,195 |

| Bitcoin | $67,037 | $67,345 |

Source: Trading Economics & Factset

Last Friday the US Supreme Court struck down the tariffs imposes by Donald Trump under the International Emergency Economic Powers Act (IEEPA) ruling them unconstitutional. The ruling was not unexpected as the power to tax lies with Congress, not the President. Not to be deterred, the President has imposed new tariffs under Section 122 of the Trade Act 1974. These tariffs are limited to 150 days and are not expected to stand up to a court challenge. How this ends is anyone’s guess now.

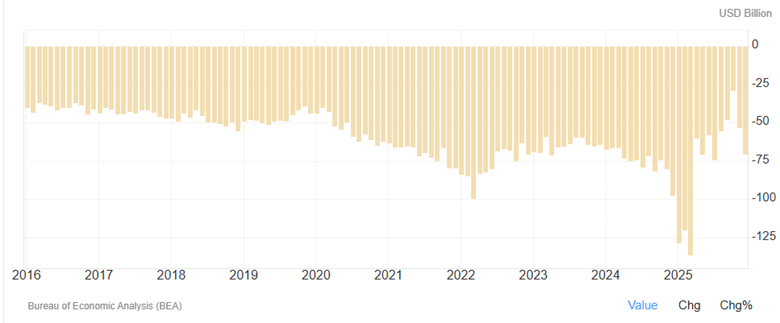

File this under irony. The US trade deficit widened in December to $70.3 billion from $53 billion in November. The trade deficit for 2025 ($901.5 billion) was virtually unchanged from 2024 ($903.5 billion). As the chart below shows much of the deficit was in the early part of the year as importers rushed to build inventories before the tariffs were imposed.

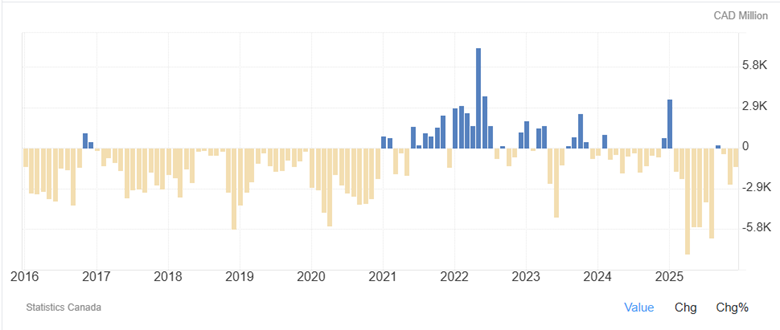

On the other hand, Canada’s trade deficit narrowed in December to $1.31 billion from $2.58 billion in November. Overall, 2025 was a mixed year with higher exports of gold and minerals while steel and aluminum took a hit. Most Canadian exports (steel & aluminum the major exceptions) to the US remain duty free under CUSMA. With CUSMA up for review/renegotiation this year, the trade picture could change dramatically.

Canada Trade Balance

Sticking with trade, Prime Minister Carney will be in India, Australia, and Japan over the next few days talking trade and security. The visit to India is getting some pushback in Canada after the 2023 assassination of a Sikh separatist in BC. In Australia, the talk will be around critical minerals. The stop in Tokyo will be to strengthen an already robust relationship.

Sometimes the market moves on fundamentals. At other times it moves on stories. This week, it was the latter as traders digested a rather dystopian piece from Citrini Research. In it, Citrini lays out a scenario (not a prediction) where AI really does decimate the white-collar workforce. As if that wasn’t unsettling enough, the timeline was short… 2028. This came on the heels of Anthropic’s moves into the realms of consultants and data providers You can find the report here.

Dystopian or not, we are starting to integrate some AI tools into select processes. (not this newsletter though – that is all me) One of the more exciting developments has been in our financial planning software (Visionworks) which we had already thought to be the best on the street. The software’s optimization functionality will now run scenarios and optimize a plan in seconds. Something that would have taken hours in the past.

We’ll close off the week with a piece from Stan Rogers celebrating the Dickensian life of white collar/tech workers…. Have a great weekend

Russ Lazaruk, RIAC, CIWM, CIM, FCSI

Managing Director & Portfolio Manager

![]()