A global assessment of cost of capital, investment cycle dynamics, and how geothermal competes for clean energy financing

The Global Investment Calculus

The central tension in geothermal finance is straightforward: the asset is exceptional once built, but the path to getting there is expensive, slow, and carries risks that most capital markets price harshly.

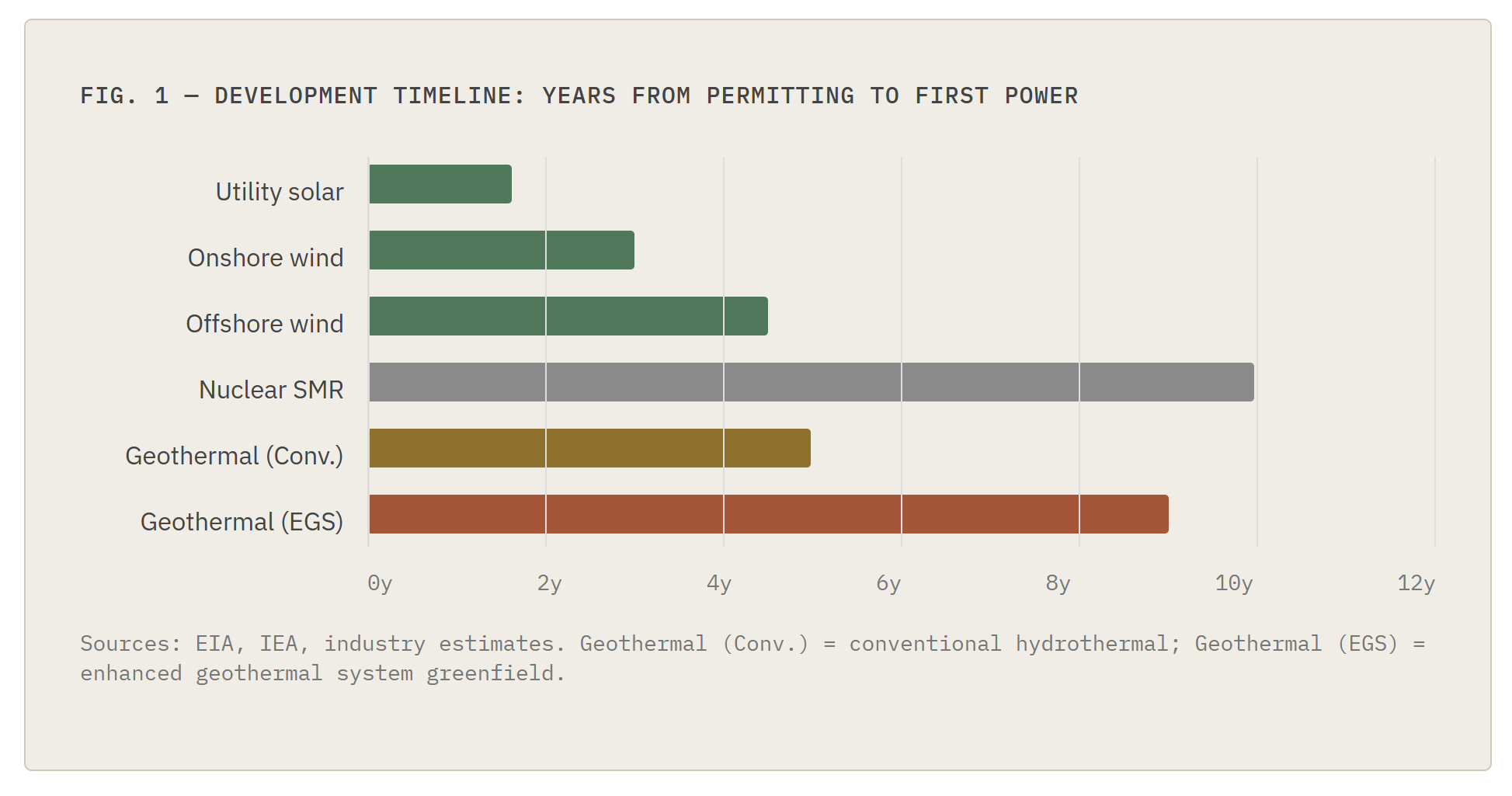

Consider the investment cycle. A conventional solar farm can move from permitting to power in 12 to 24 months. A wind project takes two to four years. A geothermal development — particularly a greenfield project — can take 7 to 10 years from initial resource assessment to first power. That timeline mismatch alone disqualifies geothermal from large categories of institutional capital that require shorter deployment windows and predictable return schedules.

The front-loading of capital is equally problematic. Exploration and drilling — the highest-risk phase of any geothermal project — must be completed before investors have meaningful certainty about what they actually own. Drilling a single well can cost $5–$10 million, and dry or underperforming wells are a genuine risk. Unlike a solar project, where cost overruns can be absorbed incrementally, a failed geothermal exploration programme can write off tens of millions of dollars with nothing to show for it.

This binary exploration risk pushes the cost of capital sharply higher in early-stage development. In East Africa, private-sector-only development of greenfield geothermal has been estimated to require returns on equity of 25%, producing levelised costs in the range of $0.14–$0.17/kWh — more than double the cost achievable through public-private partnership structures that absorb early-stage exploration risk.

Once through the exploration phase, however, the financial profile changes dramatically. A commissioned geothermal plant has negligible fuel cost, low operating expenses relative to output, a 30-to-40-year asset life, and highly predictable generation. These characteristics make it extremely bankable at the project finance level. The challenge for the industry is bridging the valley between high-risk exploration and the steady-state infrastructure asset that lenders and long-term investors prize.

LCOE and the Capacity Factor Advantage

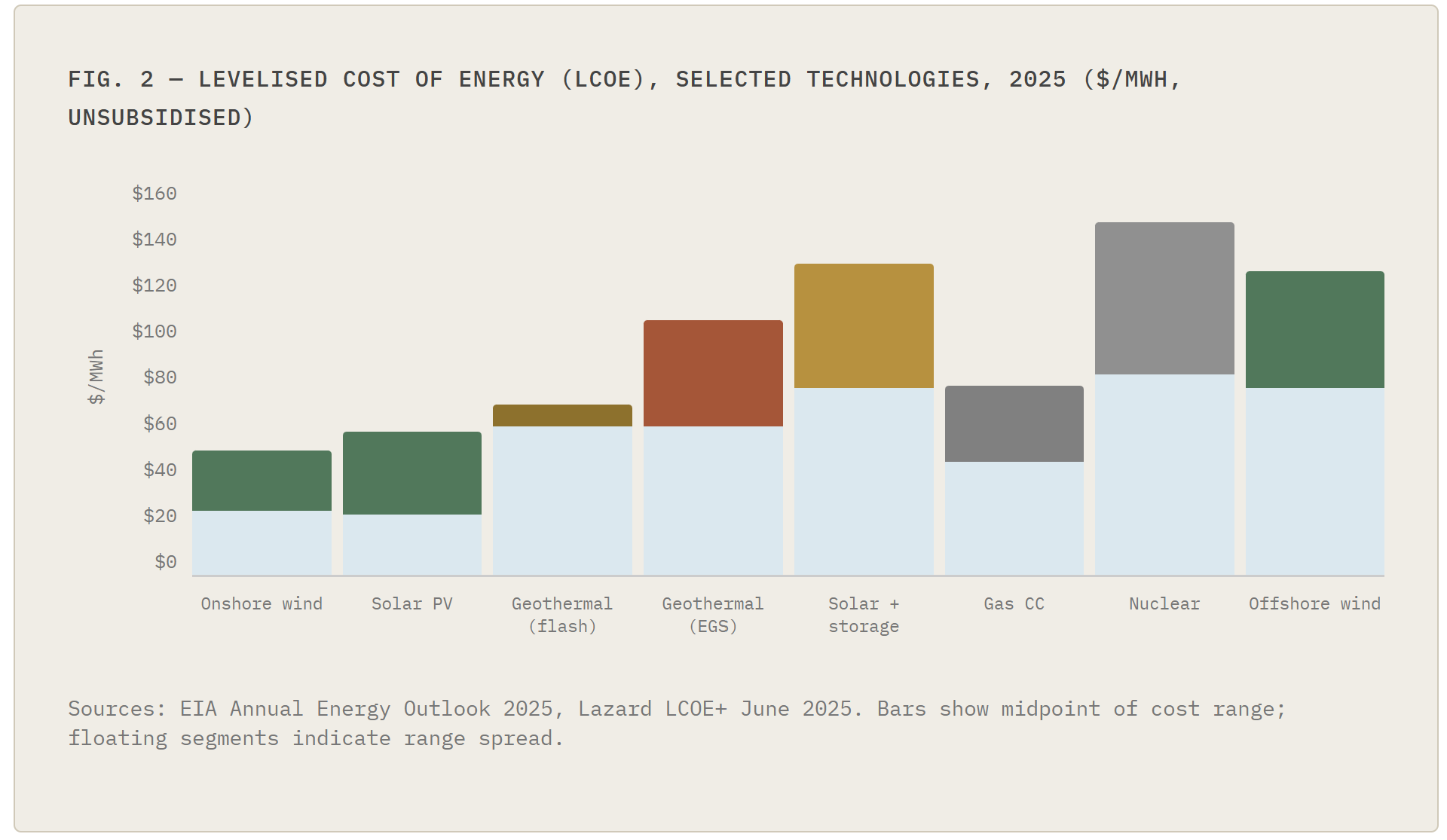

On LCOE, geothermal is competitive but not cheapest. Conventional flash plants operate at $63–$74/MWh; EGS projects are projected to reach comparable levels within the decade. Best-in-class solar and onshore wind in favourable markets undercut these figures — but LCOE comparison is misleading. It does not capture the capacity value or grid-firming premium that dispatchable generation commands.

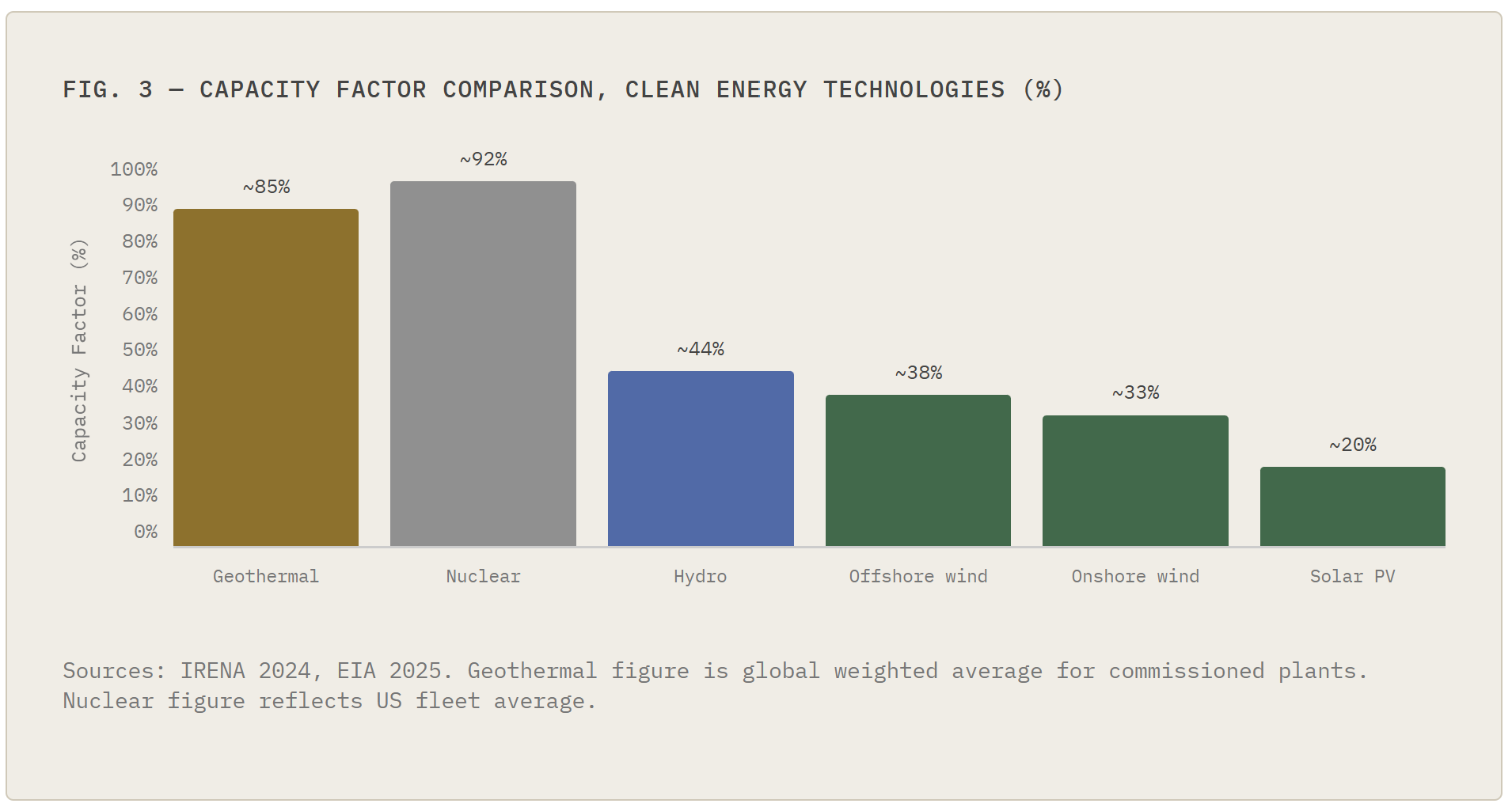

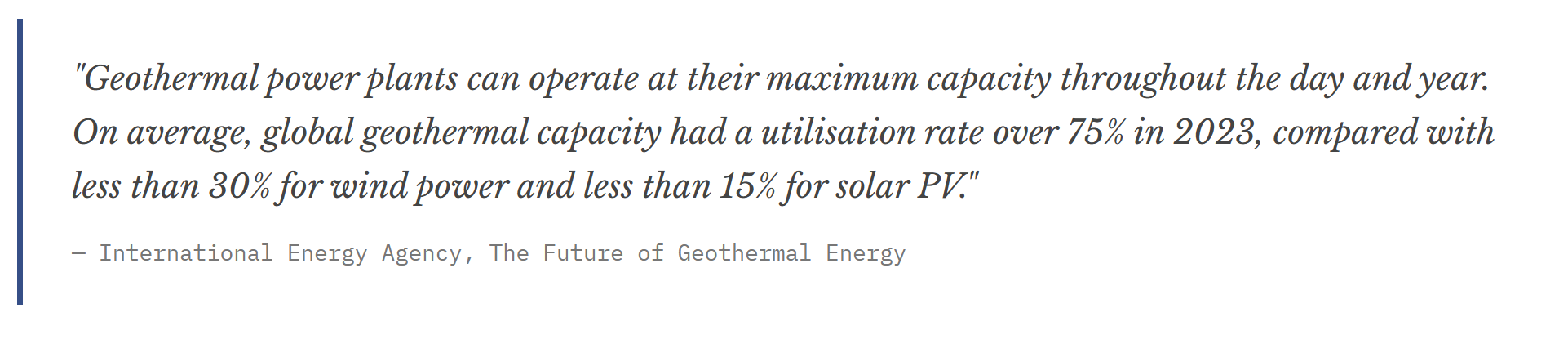

The correct comparison is geothermal against the full system cost of solar-plus-storage, where it is increasingly competitive. The capacity factor differential is stark: geothermal plants operate at 85–90%+ utilisation year-round versus 15–25% for solar and 30–40% for wind. Every dollar of installed capacity generates far more energy over the asset’s life — and commands higher capacity payments in markets that value firm, dispatchable generation.

Capital Flows and the EGS Investment Cycle

The technology that changes the investment calculus is Enhanced Geothermal Systems (EGS). By engineering reservoirs in hot dry rock rather than relying on naturally occurring hydrothermal resources, EGS unlocks geothermal’s potential almost anywhere. Drilling costs at the DOE’s Utah FORGE demonstration site fell by two-thirds between 2020 and 2023. Fervo Energy reduced its per-foot drilling costs from $1,000 to $400 between successive projects.

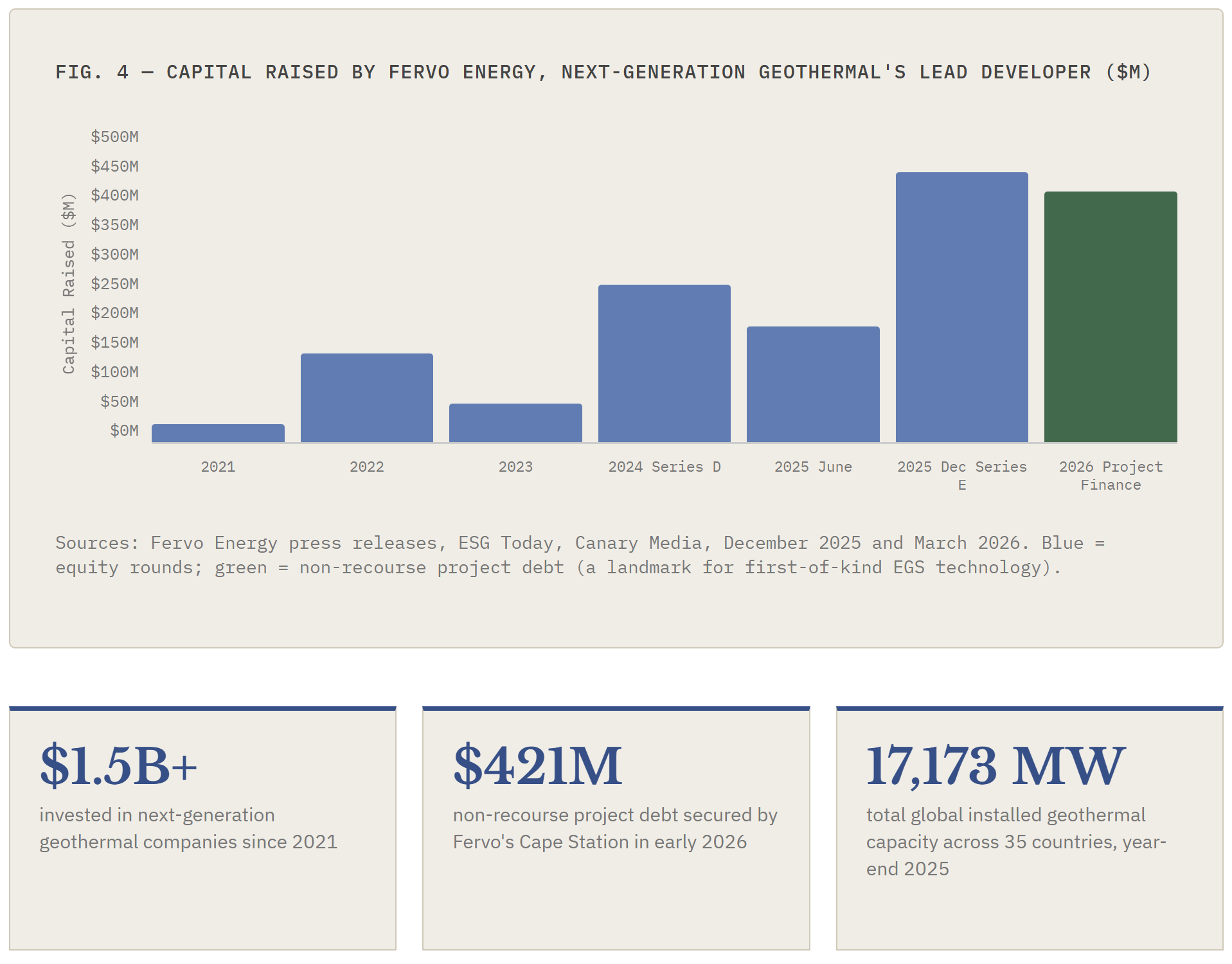

More than $1.5 billion has been invested in next-generation geothermal companies since 2021. The sector’s financing architecture is maturing: Fervo’s Cape Station project secured $421 million in non-recourse project debt in early 2026 — a landmark for a first-of-kind technology that signals the transition from venture-backed risk capital to institutional infrastructure finance. Lazard’s 2025 LCOE+ report explicitly identifies geothermal alongside SMR nuclear and long-duration storage as technologies that diverse, reliable future grids will require.

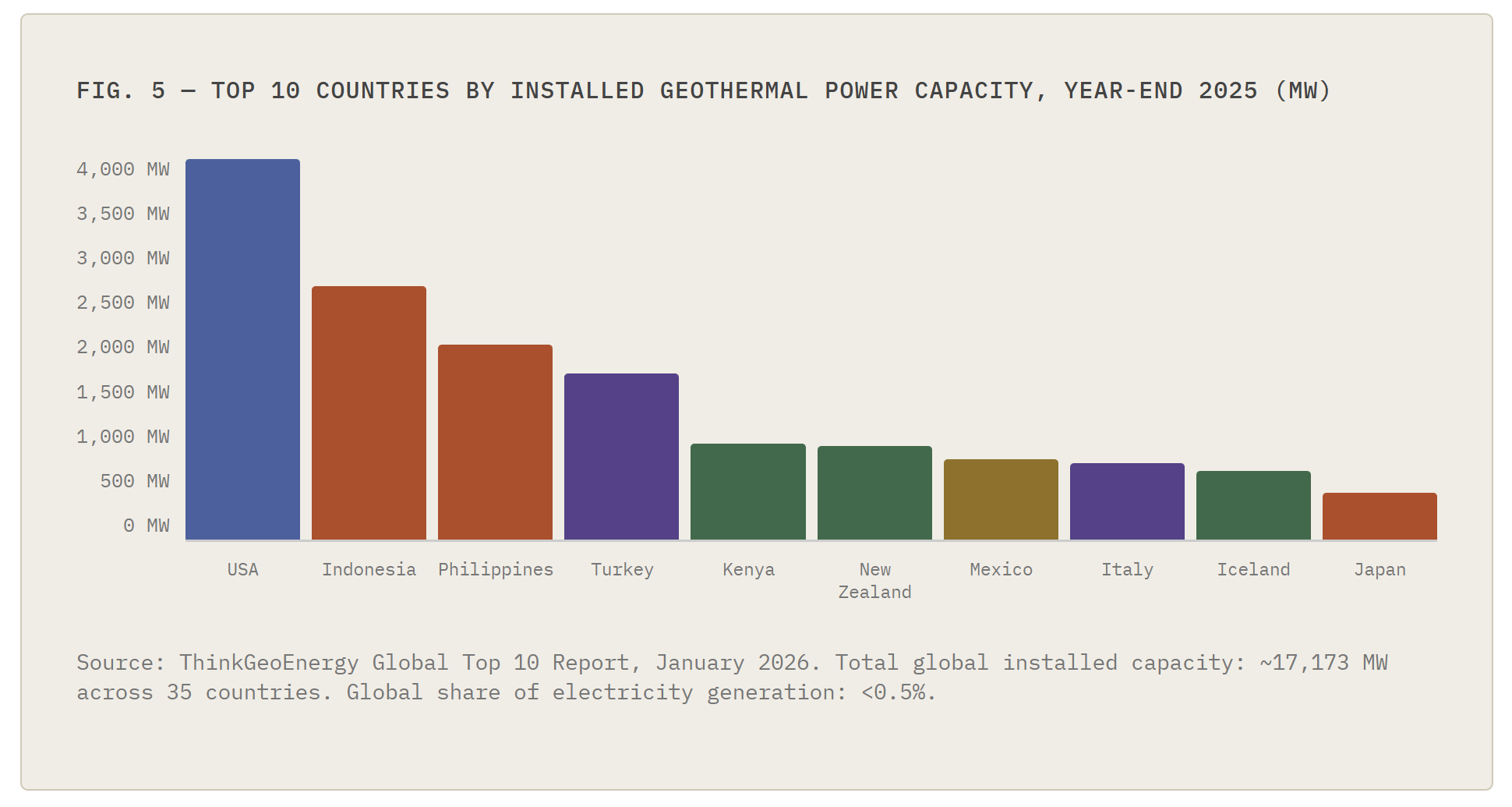

Global Installed Capacity — Current State

Regional Investment Profiles

North America: The Commercial Frontier

The U.S. is where the EGS investment thesis will be proved or disproved. The market is being driven by surging AI data centre demand, a strained grid, bipartisan political support, and a deep oil and gas services industry whose skills transfer directly to geothermal drilling. An analysis by the Rhodium Group found that enhanced geothermal could meet nearly two-thirds of new U.S. data centre demand by 2030 at costs at or below current operator rates. Corporate PPAs from Google, Meta, and others are becoming the financing backbone of the buildout, providing the long-term offtake certainty that enables project-level debt. Mexico enacted new geothermal energy laws in 2025 to streamline development, and Canada’s western provinces hold genuine resource potential and an oil and gas sector ideally positioned to pivot.

Europe: Infrastructure Capital, Not Venture Capital

Europe’s geothermal story is predominantly direct heat — decarbonising district heating networks currently running on gas. Turkey leads with nearly 1,800 MW of installed power capacity and three new plants commissioned in 2025 alone. The broader EU faces permitting timelines of five to eight years and a fragmented regulatory landscape. For investors, European geothermal is best framed as a long-dated infrastructure position: low risk once operating, predictable revenues, and a structural decarbonisation mandate that only grows stronger. The challenge is getting projects through the high-risk exploration phase in a regulatory environment that lacks the risk-sharing instruments other markets have built.

Asia: Scale, State Capital, and Strategic Opportunity

Indonesia holds the world’s largest untapped geothermal reserves at an estimated 14.6 GW and has set a target of 5.1 GW of new development by 2034, with 4.5 GW to be developed by private investors. Multilateral development banks have been essential to making projects bankable, reducing exploration risk through concessional finance structures and political risk guarantees. Development cycles of five to six years demand patient capital and specialist technical teams. The Philippines, despite comparable resources, has seen private investment stall due to the financial burden of exploration in a highly corrosive volcanic subsurface — a reminder that resource potential and investable opportunity are not the same thing.

Africa: Blended Finance or Nothing

The East African Rift System holds an estimated 17–20 GW of electricity generation capacity. Current utilisation is approximately 1 GW, almost entirely in Kenya. Private-sector-only development in high-risk sovereign environments requires equity returns of 25%, producing LCOEs of $0.14–$0.17/kWh without public support. The Geothermal Risk Mitigation Facility for East Africa covers up to 80% of exploration risks — the right model, but significantly underfunded relative to the opportunity. Climate Policy Initiative estimates that public finance for developing-country geothermal needs to increase seven to ten times its current level to mobilise sufficient private capital.

South America: Waiting for Enabling Conditions

South America’s Andes chain holds substantial geothermal resources, particularly in Chile, which has the policy framework and renewable energy ambition to develop them. High development costs, remote locations, and the absence of the exploration risk insurance mechanisms that have catalysed development elsewhere have constrained growth. The IDB’s blended finance programme offers a template, but project throughput remains well below resource assessments. Until risk-sharing mechanisms are deepened and transmission infrastructure connects remote Andean resources to load centres, South American geothermal will remain a prospective rather than active investment market.

The Competitive Capital Question

The honest assessment is that geothermal will not win a raw cost-of-capital competition against utility-scale solar or onshore wind in favourable markets. Those technologies are cheaper to build, faster to deploy, and better understood by mainstream project finance lenders. Geothermal’s investment case rests on a different argument: that as intermittent penetration rises, the grid premium on dispatchable, firm, clean baseload power will increase, and that EGS economics will improve faster than the market currently prices.

The signals investors should monitor: EGS cost trajectories; corporate PPA pricing for firm versus intermittent clean power; regulatory evolution of capacity markets in the U.S., EU, and key Asian markets; and the scaling of risk-sharing instruments in frontier markets. Fervo Cape Station’s Phase I delivery in 2026 will be a pivotal proof point for institutional capital allocation to the EGS sector broadly.

Investors who can tolerate the front-loaded capital requirements and extended development cycles will find geothermal offers something increasingly rare in the clean energy landscape: genuine differentiation, structural demand, and assets that strengthen rather than complicate the grid.

Sources: EIA Annual Energy Outlook 2025; Lazard LCOE+ June 2025; IEA, The Future of Geothermal Energy; ThinkGeoEnergy Global Top 10 Geothermal Countries, January 2026; National Laboratory of the Rockies, 2025 U.S. Geothermal Market Report; Fervo Energy press releases (June 2025, December 2025, March 2026); Climate Policy Initiative, Lessons on the Role of Public Finance in Deploying Geothermal Energy in Developing Countries; Norton Rose Fulbright, Geothermal Projects in East Africa; Rhodium Group, Enhanced Geothermal and Data Center Demand Analysis. All LCOE figures in 2024 USD unless stated. This document is prepared for informational purposes only and does not constitute investment advice.