The Week That Was

We’re publishing a bit early today to accommodate a full social schedule in Montreal. We would also like to send some of the torrential rain here back to Victoria where we haven’t had rain for over a month.

It was a generally positive week in the equity markets while the bond market had mixed results as traders debated the current inflation readings. Oil (Brent) is back over $80 as I write this and the Canadian dollar holding on to its recent strength.

It was good news on the inflation front in Canada this week, with June’s headline CPI number dropping to 2.8%. This may not be enough to satisfy the Bank of Canada though as underlying core inflation remained sticky at 3.5%. Will the Bank hike rates one more time or pause again? That is the $64 question, and there are arguments for both actions. Monetary policy does have a lag, but the labour market remains tight and pressure on wages remains in an uptrend.

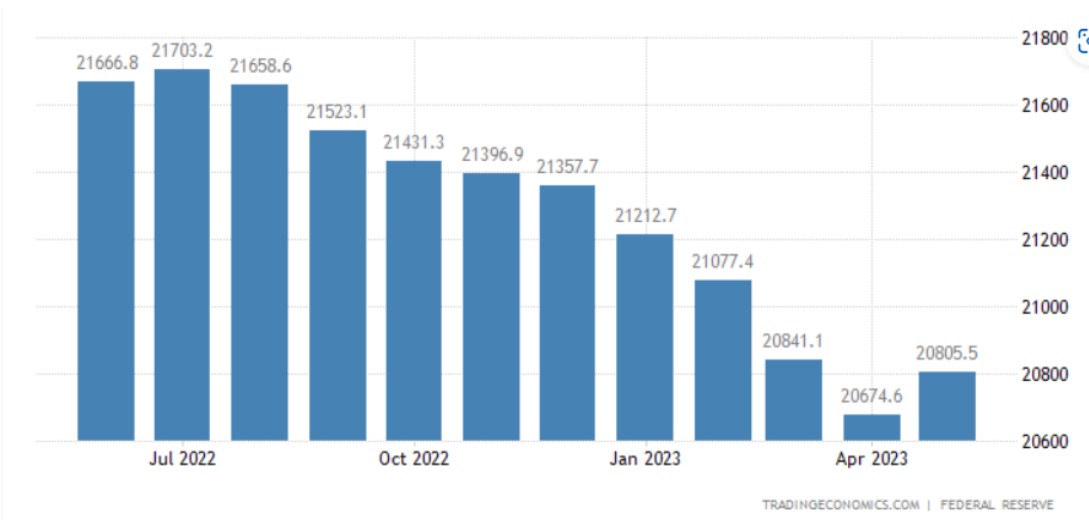

M2 money supply will be scrutinized closely this month. While not as closely watched as in years past, it is still a good indicator of the amount of liquidity in the economy. While it has fallen year over year, the May number ticked up. Traders and economists will be looking for a resumption of the downward trend.

The labour situation was brought to the fore once again in BC Ports where dockworkers rejected a mediated settlement and hit the picket lines again. The picket lines came down shortly after when they were deemed illegal as the union had not given the employers 72 hours notice. The union issued the notice then retracted it. The membership seems to be upset with the length of the agreement (4 yrs.) and want a shorter contract. Both sides will return to the bargaining table. The prospect of a legislated settlement by the federal government is a possibility if there is the prospect of extended shutdowns.

China’s latest GDP numbers point to an economy teetering on the edge of deflation. June’s Producer Prices were 5.4% lower that the previous year’s and down 0.8% month over month. Compounding the problem are ongoing problems in the real estate sector. Evergrande, the poster child for troubled property developers, reported an $81 billion loss over the past 2 years. The central government has become more reluctant to bail out insolvent private sector companies.

Remember when everyone in Europe was going to go bankrupt trying to pay their energy bills? How times change. A combination of reduced consumption and increased production from renewable sources brought wholesale prices into negative territory. Solar energy surpassed coal for the first time. A bit of a win on all fronts.

The reduced reliance on fossil fuels will no doubt get further impetus with the heat wave in Europe. A combination of climate change, El Nino, and seasonal weather patterns have large parts of the continent sweltering under45C plus temperatures. Farmers are facing drought conditions, while forest fires in Mediterranean countries are rivaling our own.

You can now read the Week that Was on our Insights page here.

I will be working from Montreal for the next few weeks where we will be celebrating the nuptials of Marc & Elise, along with a bit of time off. I’ll leave you with this piece from Beethoven in honour of the bride to be……. Enjoy

Russ Lazaruk, RIAC, CIWM, CIM, FCSI

Managing Director & Portfolio Manager

Tel 250.999.3329.

![]()