It was a mixed week on the markets with the S&P500 up slightly and a small decline in the TSX. Bond yields are virtually unchanged despite oil rising again on the ongoing closure of Hormuz. Bitcoin put in a solid performance this week making it the winner for now.

| Index | Close Apr 16th 2026 | Close Apr 24th 2026 |

| S&P500 | 7,040 | 7,101 |

| TSX60 | 34,052 | 33,705 |

| Canada 10 yr. Bond Yield | 3.50% | 3.49% |

| US 10 yr. Treasury Yield | 4.32% | 4.33% |

| USD/CAD | $1.37038 | $1.37081 |

| Brent Crude | $98.01 | $106.18 |

| Gold | $4,786 | $4,690 |

| Bitcoin | $74,934 | $77,753 |

Source: Trading Economics & Factset

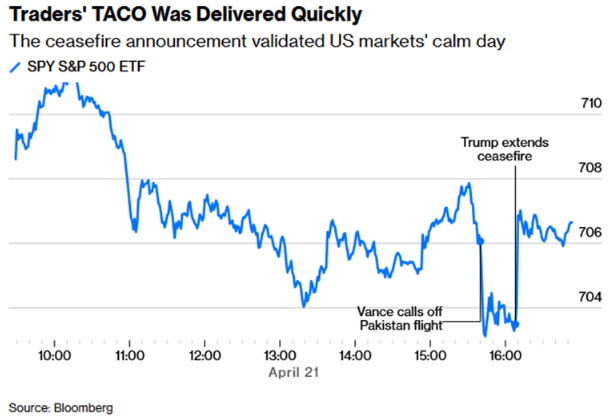

Markets have been moving on almost every pronouncement regarding the Iran War. To say it has been erratic would be an understatement. Many are discounting the TACO trade, but it appears to be a real thing as the chart below shows. Before you ask, these are virtually impossible to trade. This example was 15 minutes in duration.

Who’s really in charge? Doanld Trump likes to say that he has brought about regime change in Iran. It appears that while the players have changed the team is still intact. If anything, the Iranian Revolutionary Guard (IRGC) seem more firmly entrenched than before the attacks. The Economist though, takes a slightly more nuanced view. In a recent article it points to divisions within the leadership, exemplified by changing negotiating positions. For now, it appears that the IRGC hardliners have the upper hand.

Canada’s headline inflation popped up in March to 2.4% vs. February’s 1.8% print. The rise was almost entirely attributable to the increase in gasoline prices, up 21.2% in the month. High fuel costs also pushed up the prices of travel tours, and air fares. This was offset by declines in items such as telephone services, auto insurance, furniture, candy, and mortgage interest costs. The measures that the Bank of Canada watches were more benign. Median held steady at 2.23% and trim declining to 2.2%. There is not enough here for the Bank of Canada to move in either direction for now. That could change if or when high fuel/transport costs trickle into other goods.

South of the border, the nomination of Kevin Warsh as the new Federal Reserve Chair has been held up in the Senate. The issue is not Warsh himself, but the ongoing witch-hunt of Jerome Powell by the Trump administration. Republican Senator Thom Tillis has a key vote on the Senate Banking Committee, which is needed in the first stage of the confirmation process. He has refused to vote for any candidate until the hounds are called off of Powell. Other than that, Warsh is making the right central banker noises to get confirmed.

The Trump administration’s tariffs were struck down by the courts in March, and they were ordered to refund the $160 billion in tariffs they had collected. That process has started and companies are now applying for and receiving the refunds. However, unless there is a clear paper-trail that money will not pass down to the consumer who ultimately paid the price. As of early April, 56,000 importers had completed the necessary steps to claim the refunds online. The claims are worth an estimated $127 billion.

Things are getting testy on the Canada-US trade front again. This week, US Secretary of Commerce Howard Lutnick had some less than complimentary words for Canada and our negotiating stance. The US has also set some pre-conditions to be met before negotiations begin. PM Carney and Trade Minister Dominic Leblanc have rejected the demands. To be fair, these are things to be hashed out at the negotiating table, not surrendered before talks even start.

Staying on the CUSMA file, the Government has appointed a new advisory committee on Canada-US economic relations. The committee includes business & labour leaders, former premiers, and retired politicians such as Erin O’Toole (former leader of the CPC) and Lisa Raitt (former cabinet minister in the Harper government). The 23 members of the committee represent a broad cross section of Canadian industry and interests.

Electric Vehicle sales took a jump in Europe last month, spiking nearly 50% compared to the same period last year. Battery electric vehicles accounted for 19.4% of new vehicle registrations in the 1st quarter of 2026 compared to 15.2% for Q1 2025. The impetus is high fuel costs. Like the 1970’s OPEC oil embargo, which entrenched the drive to more fuel-efficient vehicles, this current fuel shortage is accelerating change. The longer the middle east conflict goes on, the more attractive EVs will become.

These next 2 items are related. We lost a pioneer in the investment world this week. Mark Mobius, who was instrumental in bringing the emerging markets to investors passed away in Singapore. Known as the Indiana Jones of investing, he saw opportunity where others saw risk.

As a testament to the potential of emerging markets, Greece will be upgraded by MSCI indices from an emerging to a developed market in May 2027. To be candid, Greece’s route to developed market status is a bit convoluted. It was first elevated in 2001. In 2013 it was relegated back to emerging status following the “PIIGS” financial crisis.

With thoughts of a sun soaked Aegean Sea, we’ll close off with this traditional Greek folk song… have a great weekend

Russ Lazaruk, RIAC, CIWM, CIM, FCSI

Managing Director & Portfolio Manager

![]()