A volatile week on the markets with steep selloffs early on, followed by a strong rally on Thursday. The lazy answer for the volatility is the middle east war and random social media posts from the Whitehouse. The more accurate analysis points to higher inflation and a stronger labour market. Both giving credence to rate hikes rather than cuts.

| Index | Close June 4th 2026 | Close June 11th 2026 |

| S&P500 | 7,575 | 7,389 |

| TSX60 | 35,232 | 34,658 |

| Canada 10 yr. Bond Yield | 3.44% | 3.41% |

| US 10 yr. Treasury Yield | 4.48% | 4.46% |

| USD/CAD | $1.39086 | $1.39785 |

| Brent Crude | $95.14 | $89.12 |

| Gold | $4,475 | $4,211 |

| Bitcoin | $63,565 | $63,247 |

Source: Trading Economics & Factset

This week the Bank of Canada opted to hold rates steady. Citing geo-political tensions, tariffs, a sluggish economy, and incipient inflation they are looking through the near-term issues and focused on evidence of persistent inflation.

With higher inflation, the European Central Bank (ECB) opted to raise rates by 25-bps this week. According to the Banks news release, inflation is becoming more imbedded. However, they are not establishing a pre-set course and will (as always) remain data dependent.

Newly anointed Federal Reserve Chair, Kevin Warsh, will have is work cut out for him. This week brought higher consumer prices (CPI), producer (wholesale) prices (PPI), and job creation. We’ll look at each below, but there was nothing in this week’s data to warrant a rate cut and the odds of a rate hike have grown. Which will not please the Whitehouse, where the demand for lower rates remains.

Inflation (CPI) in the US rose to 4.2%, its highest level since 2023. Core inflation was 2.9% in line with expectations. Energy (gasoline) was unsurprisingly the biggest driver of higher prices. But American consumers are also being squeezed by the higher cost of food and medical services.

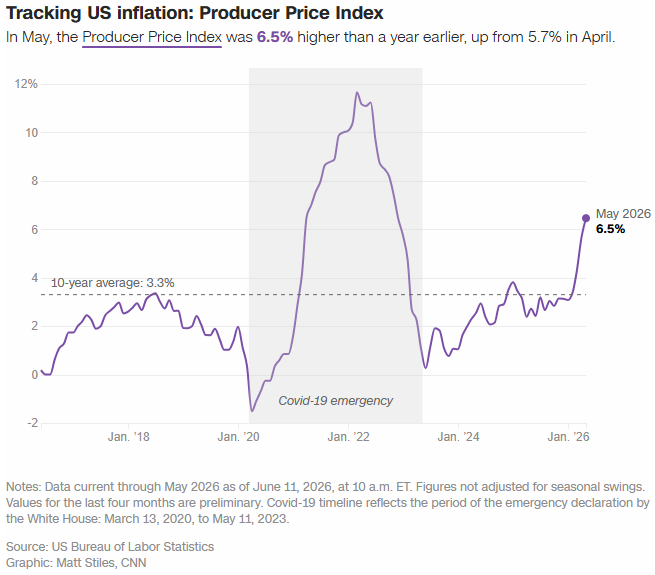

What we haven’t heard from central banks yet, is the word transient. This might be because PPI came in higher than expected at 6.5%. It is a matter of time before business start passing higher costs through to consumers. The rise in PPI is the highest since March 2022 and well above its 10 yr. average of 3.3%. Business’ choices are to eat the higher costs or pass them on to consumers. Lower profits or higher inflation.

Job creation took a jump on both sides of the 49th parallel last month. Canada added 88,000 new jobs in May well above expectations of 10,000. Better news yet, the additions were entirely concentrated in full-time work. There were 154,000 full time positions created while part-time employment shrank by 66,000 fobs. The unemployment rate fell from 6.9% to 6.6%. Wages were also up by 3% year over year.

In the US there were 172,000 new jobs created holding the unemployment rate steady at 4.3%. (note – US & Canadian unemployment rates are not directly comparable as the reporting agencies use different methodologies). Wages were also up but are lagging inflation. This is a good news / bad news story as the robust labour markets could help fuel higher inflation and interest rates. That is the part that contributed to the market sell off earlier this week.

Counter intuitively the price of oil has fall, despite renewed fighting between the US and Iran. It is often said that the best cure for high prices is high prices. Usually this means supply will rise to meet demand. This time, it appears demand has declined to meet supply. China’s oil imports have declined by 29%, due to both reduced consumption and drawing on strategic reserves that were estimated to be 1 billion barrels before the mid-east conflict.

The US, Europe, and Japan have also drawn down their strategic petroleum reserves (SPRs) giving what Carlyle’s Jeff Currie calls the abundance illusion. In this thoughtful piece he looks at the historical context of the first OPEC embargo, the political fallout, and the change in consumer behavior. His piece re-enforces my thesis that China’s demand for oil is in a secular decline thanks to their ongoing push to renewables, better technology, and the “electrification of everything”.

Trade negotiations between Canada, the US, and Mexico continue. Both Canada and Mexico have said they wish to renew the CUSMA trade treaty, while Donald Trump has indicated he’ll pursue and annual review. Canada’s trade surplus hit a new record in April ($2.7 billion) while the US continues to post trade deficits. Our trade surplus with the US was $9.5 billion the highest since February 2025.

Louise Arbour was installed as Canada’s new Governor General this week. Her career as a lawyer, Supreme Court Justice, international jurist, and UN High Commissioner for Human Rights is one to be admired.

With all things regal on our mind, we’ll close off with La Reine from Les Cowboys Fringants, chosen by our new GG to be played at her swearing in ceremony. Sara Dufour had the privilege to sing at the ceremony, but we’ll leave you with the original….. enjoy!

Russ Lazaruk, RIAC, CIWM, CIM, FCSI

Managing Director & Portfolio Manager

![]()