Not a great week on the markets but not an unmitigated disaster either. Equity and bond markets are down while oil is up sharply. High oil prices are sparking fears of inflation, leading to higher yields (lower prices) in the bond market. Both gold and Bitcoin have been volatile through the week but are not far off last Thursday’s close.

| Index | Close Mar 5th 2026 | Close Mar 12th 2026 |

| S&P500 | 6,820 | 6,675 |

| TSX60 | 33,610 | 32,841 |

| Canada 10 yr. Bond Yield | 3.35% | 3.53% |

| US 10 yr. Treasury Yield | 4.14% | 4.27% |

| USD/CAD | $1.36916 | $1.36311 |

| Brent Crude | $84.03 | $101.80 |

| Gold | $5,083 | $5,080 |

| Bitcoin | $71,211 | $70,309 |

Source: Trading Economics & Factset

The war in the Middle East is driving the markets. Not because there is a war, markets take general mayhem in their stride, but because it has effectively shut in 20%+ of the world’s oil & gas supplies. Countries outside the war zone are moving to release oil from their strategic reserves but they will not completely fill the shortfall. We’ve already seen the results of this at the pump. Airlines and shipping companies are raising prices and higher transportation costs will raise prices across a wide range of consumer goods.

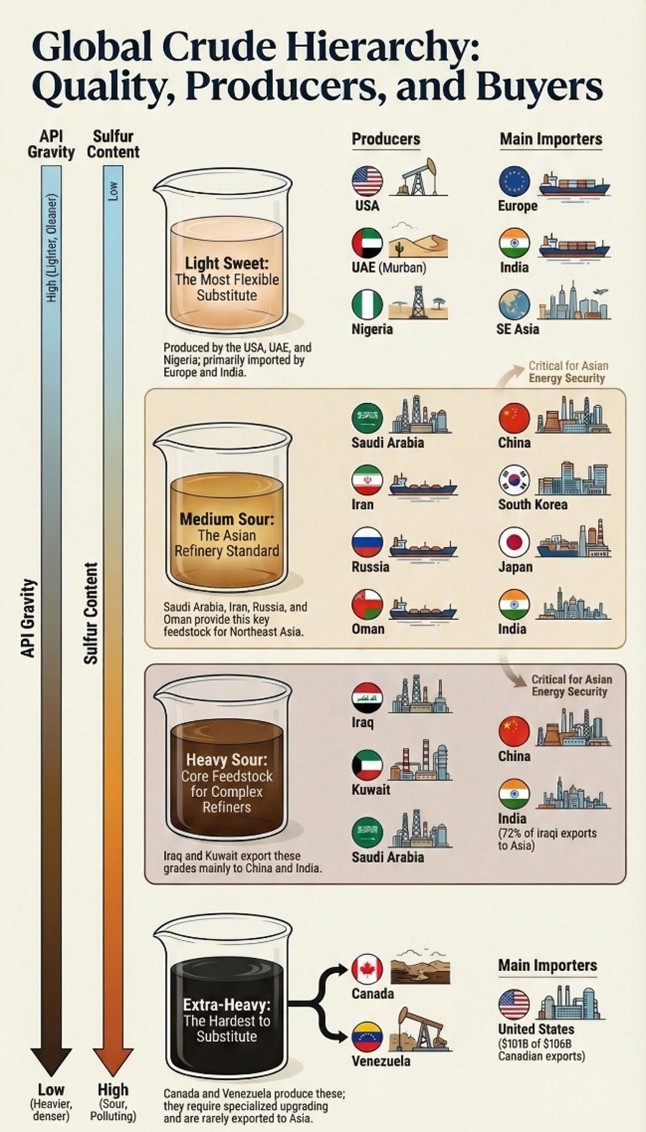

One of the issues with the interruption of supply is that oil is not as fungible as one might hope. Refineries set up to process a certain grade of crude can not easily or efficiently process a different grade, if at all. In other words, buyers of light or medium crude from the MIDDLE East can’t just switch to Canadian extra heavy crude. This chart gives a good visual of who produces what and where it is refined/consumed. Thanks to Michael Chu for the chart.

While markets look nervously at potentially higher inflation and interest rates in the future, February’s US CPI was relatively benign. The 2.4% headline number was in line with expectations and the prior month’s rate. There were some underlying pressures that are not quite so benign though. The higher PPI number has yet to work its way into consumer prices, but it is coming. Companies have worked through their pre-tariff inventories and are now starting to pass the tariff costs onto consumers. Grocery bills are climbing, especially for fruits and vegetables, while farmers grapple with higher fertilizer costs. Lower and middle-income earners are feeling the squeeze the most. The Fed will have their work cut out for them.

The US lost 92,000 jobs in February. December and January had downward revisions in their job creation numbers, December having the biggest revision, going from 48,000 new jobs to 17,000 job losses. January’s revision was a modest 4,000 swing from 130,000 gains to 126,000 gains. The softening job market coupled with the growing inflationary pressure makes stagflation a real possibility.

China posted a record trade surplus for the first 2 months of 2026. The trade balance surged from $213.6 billion compared to expectations of $179.6 billion. While exports to the US dropped by 16.9%, those to the EU rose by 19.9%. Trade also increased with the ASEAN nations by 20.3%. It wasn’t all one way; imports were also up 19.8% from the same period in 2025.

Every year our local CFA (Chartered Financial Analyst) Society puts on a joint conference with AIMA (Alternative Investment Management Association). The afternoon session is well attended and always informative. This year a lot of the talk was around the issues in the private credit market. Private credit (non-bank lending) has seen some questionable underwriting, which has led to an increase in redemption requests. This has led many funds to restrict (or gate in industry parlance) redemptions to protect remaining investors while the loans defaults are worked out.

This conversation segued into another about the need for liquidity and whether investor liquidity should be at the fund level or elsewhere in their portfolio. In this writer’s mind, potential liquidity needs should be identified as part of the goals-based asset allocation process. Allocation to illiquid or potentially illiquid investments should be sized accordingly. There is nothing wrong with private credit as an asset class, but it needs to be understood and sized appropriately. My analogy is a family office may buy an apartment building for their client family. That would never be considered a source of liquidity. The same should hold true for alternative strategies such as private credit, private equity, or infrastructure.

The weather in Victoria has gone from an early warm spring, to cool, damp, and an unexpected windstorm last night. We’ll leave you with this and hope we are back to balmy conditions next week…

Russ Lazaruk, RIAC, CIWM, CIM, FCSI

Managing Director & Portfolio Manager

![]()