Another tumultuous week on the markets. For now, the moves are being driven by the mid-east war and the Strait of Hormuz. Canada once again outperformed the US as oil (Brent) climbed back over $100 after dipping just below on Monday. Bond yields had a similar wild ride, falling as hopes for a pause took hold earlier in the week then rising again as despair reality came back to the fore.

| Index | Close Mar 19th 2026 | Close Mar 26th 2026 |

| S&P500 | 6,619 | 6,499 |

| TSX60 | 31,855 | 31,888 |

| Canada 10 yr. Bond Yield | 3.44% | 3.57% |

| US 10 yr. Treasury Yield | 4.25% | 4.43% |

| USD/CAD | $1.37421 | $1.38517 |

| Brent Crude | $107.81 | $107.58 |

| Gold | $4,650 | $4,399 |

| Bitcoin | $70,671 | $68,424 |

Source: Trading Economics & Factset

It is the fear of inflation and higher interest rates that have markets on edge. We won’t spend a lot of time on this which has been adequately covered in the press. The closure of the Strait of Hormuz is pushing up the cost of oil and gas which in turn push up inflation and interest rates. Higher interest rates (especially the 10 yr. Treasury yield) will put pressure on all asset classes. It is the discount rate and cost of carry that ultimately determine the value of asset.

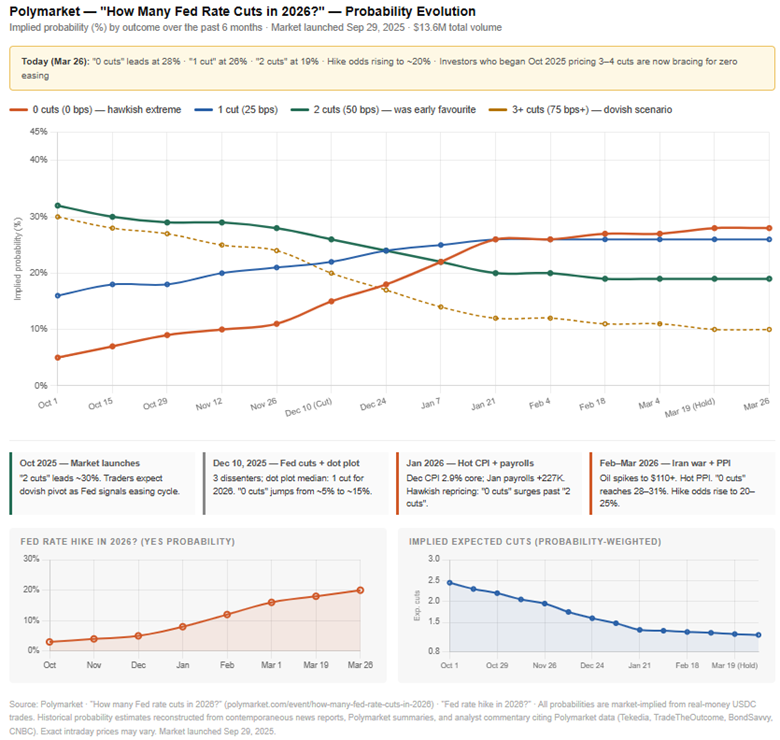

Interest rate predictions have become more hawkish. In the charts below we turn to the changes in wagers placed on Polymarket. Polymarket, for those not familiar with it, allows anyone to place a wager on virtually anything. While not necessarily predictive it does harness the wisdom or madness (depending on your point of view) of the crowd.

In a somewhat counter-intuitive move, US crude oil inventories increased in the week ending March 20th. The 2.3-million-barrel increase built on the prior weeks build of 6.6 million barrels. Expectations had been for 1.3-million-barrel decline. While oil is generally priced as a global commodity there is always a price differential between the North American benchmark price (WTI) and the global benchmark (Brent). Brent is invariably more expensive than WTI and the spread over the past year has averaged $4.80. That was until someone decided to start a war. The spread has blown out to $12.50.

Before we leave energy, we will be publishing a piece on geo-thermal energy in the next few days. While don’t currently invest in this industry, our interest is peaked as to how it may play into our thesis around the electrification of almost everything.

Meta (Facebook) and Alphabet (Google) lost a landmark court case this week. While the settlement ($3 million each) wasn’t material, the precedent is. The lawsuit, brought by a 20 yr. old woman in California, accused the companies of being legally liable for the addictive design of their platforms. This case differed from others the social media giants have faced as it addressed the underlying nature of their technology and business models, rather than the content on their sites. The results of this trial (and future appeals) could create a demand for more regulations such as the Australian ban on social media apps for youth under 16.

Last year China’s Deep Seek AI startup surprised the world with an AI model that used a fraction of the energy and computing power of current programs. This year it is Google’s AI researchers that have achieved a breakthrough. Turboquant is compression algorithm that reduces cache memory by at least 6x and increases speed by 8x (according to Google). The bottom line for the industry is less energy needed and less advanced chips for the AI data centres.

Canadian renewable energy producer Boralex has been sold. Brookfield Asset Management and La Caisse will pay $9 billion for the company with Brookfield and its subsidiaries taking a 70% stake and La Caisse 30%. The acquisition will add 4 gigawatts of energy to Brookfield’s current 46 gigawatts of renewable energy production.

Spring is officially here, though it feels like it arrived a month ago in Victoria. (Sorry rest of Canada) We’ll close off and welcome the sun with this classic from the Beatles….. enjoy!

Russ Lazaruk, RIAC, CIWM, CIM, FCSI

Managing Director & Portfolio Manager

![]()