What appears to be a boring week was anything but. Equity markets finished Thursday just below last weeks levels but there were some big swings throughout the week. Bond yields have risen as investors gauge the potential for war fueled inflation. Gold has not proven to be quite the haven some had thought but has held in over $5,000. The big move was in oil where Brent jumped over 18%.

| Index | Close Feb 26th 2026 | Close Mar 5th 2026 |

| S&P500 | 6,897 | 6,820 |

| TSX60 | 34,502 | 33,610 |

| Canada 10 yr. Bond Yield | 3.17% | 3.35% |

| US 10 yr. Treasury Yield | 4.01% | 4.14% |

| USD/CAD | $1.36673 | $1.36916 |

| Brent Crude | $70.85 | $84.03 |

| Gold | $5,195 | $5,083 |

| Bitcoin | $67,345 | $71,211 |

Source: Trading Economics & Factset

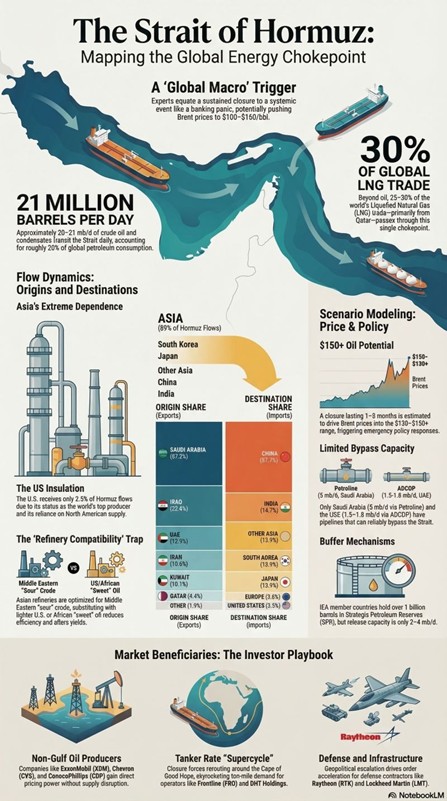

For someone who covets the Nobel Peace Prize Donald Trump has a very odd way of trying to earn it. Saturday saw the start of the latest Middle East war as Israeli and US forces struck strategic sites in Iran. One of the early Iranian casualties was its Supreme Leader Ayatollah Ali Khamenei. We won’t spend a lot of time analyzing the war or its causes other than to note that for both Israel and the Iranian regime it is existential, so we don’t expect it to end soon or easily.

From a financial markets viewpoint, the widening of the war to include neighbouring Gulf states and the closure of the Straits of Hormuz are critical areas of risk. 20-25% of the world’s seaborne oil and 20% of the world’s seaborne LNG passes through the Straits of Hormuz. But it is not just energy in jeopardy. 26 million containers and 1/3 of the world’s nitrogen fertilizers pass through this chokepoint. For now, the Strait is essentially closed to commercial traffic. As we know from the Pandemic, supply chain disruptions can trigger inflation. Barring permanent or long-term damage to the infrastructure (ports, refineries, etc.) the inflation should be transitory.

Asian markets have not taken the closure of Hormuz lightly. They are heavily reliant on the Middle East for energy and logistics. The Korean markets took the news the hardest selling off close to 20%.

China has set their GDP target for 2026 at a record low of 4.5%-5%. This is the 1st time since 1991 the target has been below 5%. The low target reflects several realities including a population that is now shrinking rather than growing, a slowdown in the housing markets, and the transition from an export led to a consumer centric economy.

Artificial Intelligence developer Anthropic has been in the news after they refused to drop the guardrails on their technology at the behest of the Pentagon. The company had insisted their technology not be used for autonomous weapons. Part of their reasoning was the tech is not developed enough to be entrusted with a weapons system. They also refused to let it be used for mass surveillance. The Pentagon has labeled the company a “supply chain risk”, which will freeze them out of defence related work.

The US Producer Price Index (PPI) was higher than expected in January. Both core and headline numbers were well ahead of expectations. We’ll see how long it takes for these numbers to make their way to the consumer.

In Canada 4th quarter GDP in 2025 fell 0.6% (annualized) which was below expectations of a flat number. There is (surprise) some nuance to the number. After building up inventories early in the year, companies spent the last quarter drawing them down, which does not contribute to GDP. Those inventories will need to be rebuilt, so will give a lift to 2026 GDP growth.

We’ll close off here with a special request from “JJ” in Saskatchewan (I feel like a radio DJ here)…. Have a great weekend,

Russ Lazaruk, RIAC, CIWM, CIM, FCSI

Managing Director & Portfolio Manager

![]()